Most adults struggle with managing money and building wealth sustainably, often feeling overwhelmed by conflicting advice and complex financial jargon. Financial independence requires both financial literacy and multiple income streams working together. This guide covers practical steps to improve financial habits, diversify income sources, and invest smartly using research-backed strategies that actually work. You'll learn behavior-driven techniques that make managing money easier and discover how to build lasting wealth through disciplined action and smart choices.

Table of Contents

- Key takeaways

- Understanding the foundation: key principles for financial intelligence

- Preparing your financial toolkit: essential materials and resources

- Executing your plan: step-by-step strategies to diversify income and invest wisely

- Troubleshooting and common mistakes: how to stay on track financially

- Discover tools to boost your financial journey

- Frequently asked questions about becoming financially smart

Key Takeaways

| Point | Details |

|---|---|

| Habit driven investing | Financial success comes from building consistent routines, such as tracking expenses, automating transfers, and following 12 week plans rather than relying on willpower. |

| Diversify income streams | Diversifying income reduces risk and strengthens financial independence by blending wages, investments, and other revenue sources. |

| Automation and cooldowns | Automating savings and bill payments reduces decision fatigue and curbs impulsive purchases with a clear cooldown policy. |

| Global equity diversification | Expanding beyond domestic equities can improve long term returns and reduce risk compared with relying on lifecycle funds. |

Understanding the foundation: key principles for financial intelligence

Financial intelligence begins with understanding your money habits and the psychology behind every spending decision you make. Most people fail financially not because they lack knowledge, but because they struggle with consistent execution. Your brain's reward system pushes you toward immediate gratification, making delayed rewards like retirement savings feel less compelling than that new gadget.

Budgeting and saving are foundational for building wealth and require consistent discipline that most traditional advice overlooks. Instead of relying on willpower alone, build habits via 12-week plans that include tracking every expense, automating key financial tasks, and establishing clear rules for spending decisions. This behavioral approach beats theoretical knowledge every time.

Consider these core principles:

- Track every dollar for at least 12 weeks to identify spending patterns and leaks

- Automate savings transfers immediately after payday to remove decision fatigue

- Establish a 24-hour cooldown rule for purchases over $100 to prevent impulse buying

- Review your financial dashboard weekly to maintain awareness and motivation

- Set specific, measurable goals rather than vague intentions like "save more"

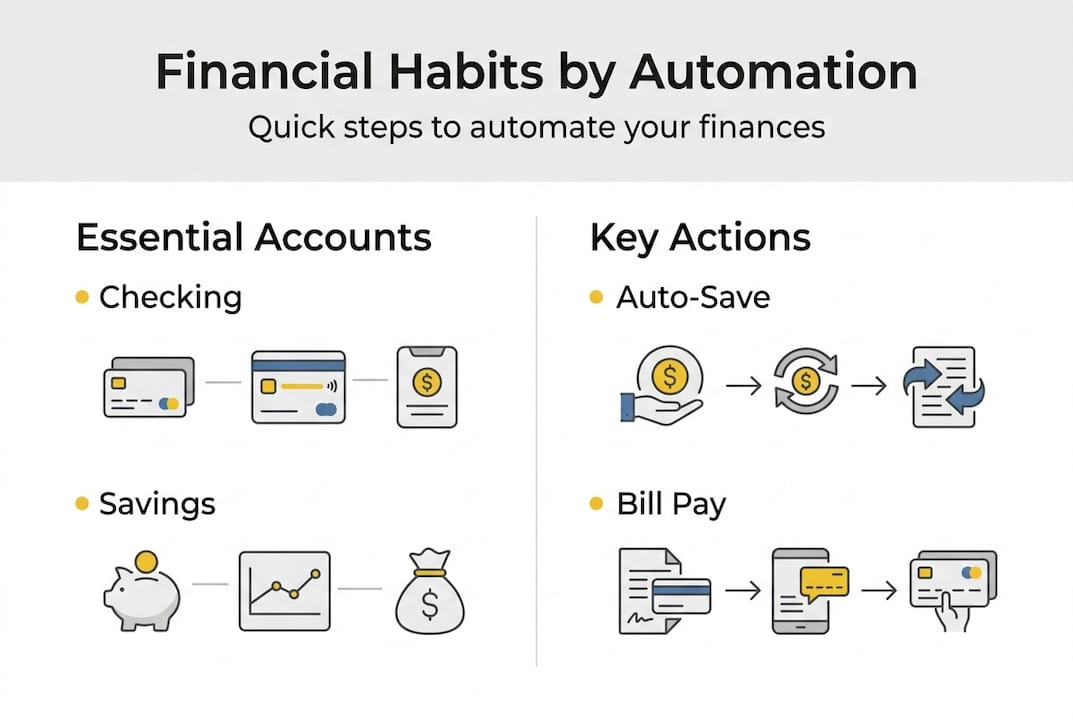

Automation of savings and bills reduces errors and builds saving habits effortlessly without requiring constant mental energy. When you automate your finances, you leverage technology to overcome human weakness. Your checking account automatically sends money to savings, investments, and bill payments before you can spend it elsewhere.

Pro Tip: Create separate savings accounts for different goals like emergency fund, vacation, and home down payment. Seeing progress in multiple buckets provides psychological wins that keep you motivated through the long journey to financial independence.

The psychology of money matters more than math. You already know you should save and invest, but knowing doesn't equal doing. Behavioral fixes like implementing financial literacy fundamentals through systematic habit formation create lasting change. Focus on building systems that work with your psychology, not against it.

Preparing your financial toolkit: essential materials and resources

Before executing any financial strategy, you need the right accounts and tools in place to manage money effectively. Think of this as assembling your financial command center where all decisions and actions flow through organized channels.

Necessary accounts include checking for daily transactions, high-yield savings for emergency funds, retirement accounts like 401(k) or IRA for tax-advantaged growth, and taxable investment accounts for additional wealth building. Each account serves a specific purpose in your overall financial architecture.

| Account Type | Primary Purpose | Recommended Provider Features |

|---|---|---|

| Checking | Daily transactions and bill payments | No monthly fees, robust mobile app, instant transfers |

| High-yield savings | Emergency fund (3-6 months expenses) | Competitive interest rate above 4%, FDIC insured |

| Retirement (401k/IRA) | Tax-advantaged long-term growth | Low-fee index fund options, employer match availability |

| Taxable investment | Additional wealth building beyond retirement limits | Commission-free trading, fractional shares, automatic investing |

| Health Savings Account | Medical expenses with triple tax advantage | Investment options after minimum balance, no fees |

Budgeting apps, automated transfers, and tracking spreadsheets streamline financial management by consolidating information and reducing manual work. Popular apps sync with your accounts to categorize spending automatically, though you should review categories weekly to ensure accuracy. Some people prefer spreadsheets for greater customization and control.

Understand tax-advantaged accounts and how they support wealth building through either tax-deferred growth or tax-free withdrawals. Traditional IRAs and 401(k)s reduce your taxable income now but you'll pay taxes on withdrawals in retirement. Roth accounts use after-tax dollars but grow and withdraw tax-free. Health Savings Accounts offer triple tax benefits when used for medical expenses.

Access to educational materials and communities aids continuous learning and motivation throughout your financial journey. Consider these resources:

- Personal finance books focusing on behavioral psychology and practical implementation

- Online communities where members share real experiences and accountability

- Financial podcasts for learning during commutes or workouts

- Courses covering specific skills like tax optimization or real estate investing

- Mentors or advisors who've achieved the financial goals you're pursuing

Your toolkit should evolve as your financial situation grows more complex. Start simple with basic checking, savings, and retirement accounts, then add specialized tools as you develop multiple income streams and investment strategies. The key is having everything ready before you need it, so opportunities don't slip away while you're setting up accounts. Explore financial tools and products designed to simplify this preparation phase.

Executing your plan: step-by-step strategies to diversify income and invest wisely

Creating multiple income streams reduces risk and accelerates financial independence by ensuring you're not dependent on a single source of money. If one stream dries up, others continue flowing. This diversification principle applies to income just as much as investments.

Follow this stepwise approach to building income diversity:

- Secure your primary income by excelling at your main job and documenting your achievements for raises and promotions

- Identify skills you can monetize through freelancing or consulting in evenings and weekends

- Create digital products like courses, ebooks, or templates that generate passive income after initial creation

- Invest in dividend-paying stocks or real estate investment trusts for regular cash flow

- Build online businesses or content platforms that scale beyond trading time for money

- Automate income collection and tracking so you maintain visibility across all streams

For investing, the conventional wisdom of lifecycle funds deserves scrutiny. While convenient, lifecycle funds may not be optimal for investors with long time horizons. Research suggests that all-equity international diversification often provides higher expected utility, especially when you have decades before needing the money.

| Investment Approach | Risk Level | Expected Return | Best For |

|---|---|---|---|

| Lifecycle/Target-Date Funds | Decreases over time | Moderate, conservative near retirement | Hands-off investors prioritizing simplicity |

| All-Equity International Index | Higher, consistent | Higher long-term growth potential | Long-horizon investors comfortable with volatility |

| Balanced Portfolio (60/40) | Moderate, stable | Moderate with reduced volatility | Mid-term goals or moderate risk tolerance |

| Individual Stock Selection | Varies widely | Unpredictable, often underperforms indexes | Experienced investors with time for research |

The key insight is that lifecycle funds automatically shift toward bonds as you age, reducing potential returns precisely when compound growth matters most. If you have 20 or 30 years until retirement, maintaining higher equity exposure through globally diversified index funds may serve you better.

Use automation and behavioral rules to maintain consistency in investing and income management regardless of market conditions or emotional impulses. Set up automatic monthly investments that continue whether markets rise or fall. This dollar-cost averaging removes the impossible task of timing the market.

Pro Tip: Treat your side income streams as serious businesses by tracking expenses, setting revenue goals, and reinvesting profits for growth. The difference between a hobby and an income stream is intentional management and scalability.

Diversification works when streams are truly independent. A full-time marketing job plus freelance marketing consulting isn't real diversification since both depend on the same industry and skills. Better combinations pair employment with real estate income, or consulting with digital product sales. Learn more about investment and income diversification strategies that create genuine independence.

Troubleshooting and common mistakes: how to stay on track financially

Even with solid plans and good intentions, most people encounter predictable obstacles that derail financial progress. Recognizing these patterns early helps you course-correct before small mistakes become major setbacks.

Common mistakes include emotional spending triggered by stress or celebration, ignoring diversification by keeping all money in one investment or income source, and failing to automate finances which leads to missed payments and lost opportunities. These errors stem from human psychology, not lack of intelligence.

Cooldown periods before financial decisions reduce impulsivity and bad choices significantly. Behavioral fixes like cooldowns prove more effective than simply knowing what you should do. Implement a mandatory 24-hour waiting period for purchases over $100, and a 7-day period for purchases over $1,000. This simple rule prevents countless regrettable transactions.

Regular review and adjustment of budgets and investment allocations keep plans aligned with changing goals and circumstances. Schedule monthly money meetings with yourself or your partner to review:

- Actual spending versus budgeted amounts across all categories

- Progress toward savings and investment goals with specific metrics

- Performance of income streams and opportunities for optimization

- Upcoming large expenses requiring preparation or adjustment

- Changes in financial goals or life circumstances affecting priorities

Avoid these specific pitfalls:

- Lifestyle inflation that consumes every raise or bonus before you can save it

- Paralysis from information overload instead of taking imperfect action

- Comparing your financial journey to others' highlight reels on social media

- Abandoning your entire plan after one slip-up or unexpected expense

- Neglecting to celebrate progress milestones along the multi-year journey

Treat setbacks as learning opportunities and avoid all-or-nothing thinking that destroys momentum. One expensive dinner doesn't ruin your budget any more than one salad makes you healthy. What matters is the pattern over weeks and months, not individual decisions.

Pro Tip: Create a "mistakes journal" where you document financial errors and the emotions or circumstances that led to them. Patterns emerge quickly, revealing your specific triggers and weak points. This self-awareness becomes your strongest defense against repeating expensive mistakes.

When you notice yourself off track, resist the urge to give up entirely. Instead, analyze what happened without judgment, adjust your systems to prevent recurrence, and restart immediately. The difference between financial success and failure often comes down to how quickly you recover from inevitable mistakes. Discover financial mistake prevention tools that help you maintain consistency even when life gets chaotic.

Discover tools to boost your financial journey

You've learned the principles and strategies for building financial intelligence, but implementing them consistently requires support and resources designed for real-world application.

CrownLeaf offers curated financial tools and educational resources aligned with smart money management that bridges the gap between knowing and doing. Whether you're just starting your financial literacy journey or optimizing multiple income streams, having expert-backed solutions makes the process manageable rather than overwhelming.

Explore products that help automate savings, streamline investment decisions, and track multiple income streams efficiently so you spend less time managing money and more time building wealth. The right tools transform complex financial management into simple daily habits.

Benefit from expert-backed solutions that make financial literacy and independence achievable for people at every stage of their journey. Visit CrownLeaf financial products to discover resources specifically designed to support the strategies you've learned in this guide.

Frequently asked questions about becoming financially smart

What is the quickest way to improve financial literacy?

Start with a 12-week habit-building plan that tracks every expense and automates your savings. Behavioral approaches like cooldown rules for purchases and automated transfers create faster results than reading theory alone. Focus on doing rather than learning more, since action builds both skills and confidence simultaneously.

How many income streams should I aim for?

Most financially independent people maintain 3 to 5 truly diversified income streams that don't depend on the same industry or time investment. Start with your primary job, add one skill-based side income, then build passive streams through investments or digital products. Quality and sustainability matter more than quantity, so master each stream before adding another.

Are lifecycle funds a good choice for beginners?

Lifecycle funds offer simplicity and automatic rebalancing, making them decent starting points for hands-off investors. However, research shows that all-equity international diversification often delivers higher expected utility for long-term investors who can tolerate volatility. If you have 20+ years until retirement, consider maintaining higher equity exposure rather than automatically shifting to bonds.

How does automation help with financial habits?

Automation removes decision fatigue and human error by executing financial tasks without requiring willpower or memory. When savings transfers, bill payments, and investments happen automatically, you eliminate the opportunity to spend that money elsewhere. This systematic approach builds wealth consistently regardless of motivation or busy schedules.

What's the best approach to avoid impulsive spending?

Implement a mandatory 24-hour cooldown period for purchases over $100 and a 7-day waiting period for purchases over $1,000. This behavioral rule disrupts the emotional impulse and gives your rational brain time to evaluate whether the purchase aligns with your goals. Most impulse purchases lose their appeal after the waiting period expires.